Understanding Section 16 Filings: Forms 3, 4, and 5 Explained

Section 16 of the Securities Exchange Act of 1934 requires certain insiders to report their ownership of and transactions in company equity securities. If you’re an officer, director, or major shareholder of a public company, you likely have Section 16 reporting obligations, and the SEC expects timely and accurate filings.

This post explains the basics of Section 16, when each form is required, and how ACN can help.

What Are Section 16 Filings?

Section 16 filings are SEC reports – Forms 3, 4, and 5 – that certain corporate insiders must submit to publicly disclose their ownership and transactions in company equity securities. They are filed electronically through EDGAR and are freely accessible to the public.

What Is Section 16?

Section 16 is a set of SEC rules requiring company insiders to disclose their holdings and transactions in the securities of their own company. The rules promote transparency and help deter insider trading.

Why Was Section 16 Created?

Section 16 was enacted as part of the Securities Exchange Act of 1934, in the wake of the Great Depression, when insider trading was rampant. Congress included it to limit the advantages that senior officers and directors had when trading their own company’s stock – particularly the ability to profit from short-swing transactions (matching purchases and sales within a six-month window). Section 16(b) requires insiders to disgorge any profits from such short-swing trades back to the company, regardless of intent.

Who Must File?

Covered individuals include:

Directors of a public company

Officers of a public company (as defined by Rule 16a-1(f))

Beneficial owners of more than 10% of any class of a company’s registered equity securities

What Counts as Beneficial Ownership?

Beneficial ownership is one of the most commonly misunderstood aspects of Section 16. You don’t have to physically hold equity yourself to be covered:

If your spouse or household member is a beneficial owner, you may also be subject to Section 16.

If you hold 10% or more through a group or entity (even without reaching that threshold individually), Section 16 still applies.

Indirect ownership – through trusts, partnerships, or controlled entities – must be reported.

Misinterpreting beneficial ownership is one of the most common compliance mistakes filers make. If you’re unsure whether you’re covered, consult a compliance professional or securities counsel.

These insiders must report their initial ownership, as well as any changes to their holdings, through the SEC’s EDGAR system using Form 3, Form 4, or Form 5.

What Are Forms 3, 4, and 5?

Here’s a breakdown of each form and when it’s required:

Section 16 Forms at a Glance

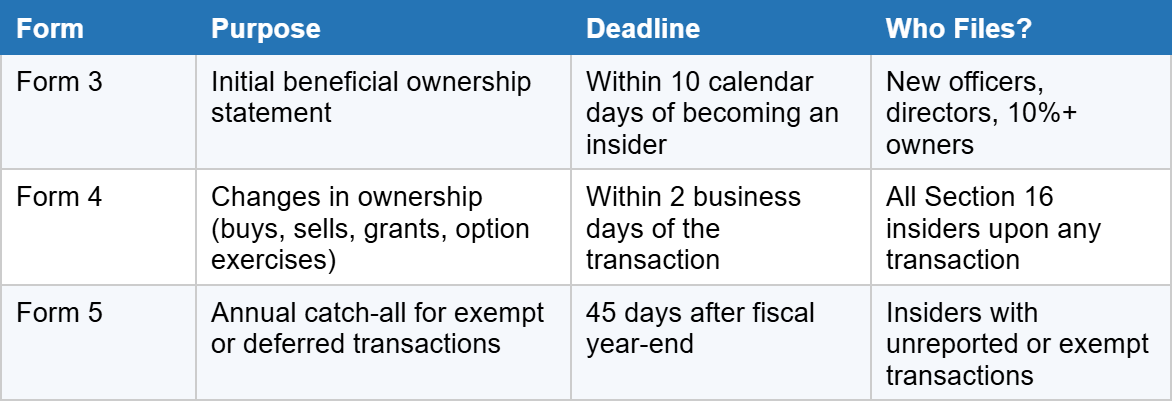

Form 3 – Initial Statement of Beneficial Ownership (official SEC form)

This is the first form insiders must file when they become subject to Section 16 – for example, upon becoming an officer, director, or 10% owner.

Deadline: Within 10 calendar days of becoming a reporting insider.

Key Components of Form 3

For each class of equity security, Form 3 requires insiders to report:

Security Title –the class or title of the security (e.g., common stock, restricted stock, stock options)

Amount Beneficially Owned – the number of securities owned as of the filing date

Nature of Ownership – whether ownership is direct or indirect (through a spouse, trust, or controlled entity)

Note: Most insiders are required to file a Form 3 even if they do not beneficially own any reportable securities at the time they become subject to Section 16. In such cases, the form is filed to establish reporting status.

Form 4 – Statement of Changes in Beneficial Ownership (official SEC form)

Used to report changes in insider ownership – for example, buying or selling stock, exercising options, or receiving stock grants.

Deadline: Within 2 business days of the transaction date.

What Transactions Require Form 4?

Form 4 is the most frequently filed Section 16 form. It must generally be filed for any of the following:

Open-market purchases or sales of company stock

Stock option exercises

Vesting of restricted stock or RSUs (when it results in a reportable change in beneficial ownership, such as share delivery or tax withholding transactions)

Sales under Rule 10b5-1 trading plans

Equity grants received from the company

Transfers to or from a trust or other indirect holding

Transactions in company stock by a partnership in which the insider is a member

In general, most changes in beneficial ownership must be reported using the appropriate transaction code, even if purchases and sales have balanced out with no net change in holdings.

Tip: When calculating the two-business-day deadline, account for U.S. federal holidays – EDGAR does not accept filings on those days.

Form 5 – Annual Statement of Beneficial Ownership (official SEC form)

A year-end catch-all used for transactions that were exempt from Form 4 reporting or were eligible for deferred reporting.

Deadline: By 45 days after fiscal year-end (typically February 14 for calendar-year companies).

Can You Skip Filing Form 5?

Insiders are not required to file Form 5 if all reportable transactions have already been timely reported on Form 3 or Form 4, and there are no transactions eligible for deferred reporting.

To avoid a Form 5 filing:

Transactions eligible for deferred reporting may be voluntarily reported earlier on Form 4.

Late transactions should be reported promptly via an amended or late Form 4.

Any omissions in initial holdings should be corrected through an amended Form 3.

If no unreported or deferred transactions exist as of fiscal year-end, Form 5 is not required.

What Transactions May Be Exempt from Form 4 Reporting?

Not all transactions require immediate reporting on Form 4. Some transactions are exempt from Section 16(a) short-term reporting but may still be reportable on Form 5. Common exemptions include:

Purchases under a Section 423 employee stock purchase plan (ESPP)

Routine transactions under qualified 401(k) and other tax-qualified plans

Certain transfers under domestic relations orders (e.g., divorce settlements)

Gifts of securities (which may be reportable on Form 5 instead of Form 4)

Even “exempt” transactions may still need to be disclosed on Form 5. If you’re unsure whether a transaction requires reporting, consult a compliance professional or securities counsel.

Do These Forms Ever Require Amendments?

Yes – if there’s a material error in a previously filed Form 3, 4, or 5 (such as an incorrect number of securities or wrong transaction code), the filer must submit an amended version with the correct information.

Amended filings must clearly note the correction and reference the original filing. ACN can assist with amendment filings when needed, though the filer is responsible for identifying what needs to be corrected.

What Happens If You Miss a Deadline?

Missing a Form 4 deadline can result in public disclosure of the failure in the company’s annual proxy statement, as well as increased scrutiny from regulators. Section 16 reporting is time-sensitive – and noncompliance is easily visible to investors and regulators alike.

How ACN Can Help

ACN makes it easy to file Forms 3, 4, and 5 on time and without hassle. Whether you’re filing as an individual insider or on behalf of a client, we handle the submission logistics so you can focus on what matters.

Here’s what you get:

Simple templates for Forms 3, 4, and 5 – modeled after the official SEC versions, easy to complete

Fast turnaround – most filings completed and submitted within 24 hours

Proof for review before submission – you receive an HTML copy of the report to approve before it’s filed with the SEC

Accurate EDGAR submission – you’ll need a CIK number and EDGAR credentials, and will need to add ACN as a delegated filer in EDGAR, but we handle the formatting and submission from there

Support for initial, ongoing, and annual filings – we assist with all Section 16 filing types, including occasional amendments

Whether you’re filing for yourself or managing filings for others, ACN is a reliable partner. We work directly with individual insiders and the compliance or legal firms that need a responsive, experienced team to handle Section 16 obligations.

Frequently Asked Questions

Do Section 16 filings cost anything to file with the SEC?

No. Section 16 filings (Forms 3, 4, and 5) do not require a filing fee with the SEC. However, you do need EDGAR access codes (a CIK number and login credentials) to submit. ACN handles the filing on your behalf – you just need to supply the access codes the first time.

Are Section 16 filings public?

Yes. Once filed through EDGAR, Section 16 filings are publicly accessible – indefinitely. Companies are also required to post Forms 3, 4, and 5 on their corporate website by the end of the next business day after filing, where they must remain accessible for at least 12 months.

Can I file a paper Form 4?

No. The SEC no longer accepts paper filings of Forms 3, 4, and 5 except in rare cases where a hardship exemption is granted. Electronic filing through EDGAR is mandatory for all Section 16 reports.

What if two people beneficially own the same securities?

When more than one person subject to Section 16 is deemed to be a beneficial owner of the same equity securities, all such persons must report – either separately or jointly. A single Form 3, 4, or 5 may be filed on behalf of all persons in a group where holdings are aggregated.

What is a “short-swing profit” and why does it matter?

Under Section 16(b), insiders who buy and sell (or sell and buy) the same company’s securities within any six-month period may be required to return any resulting profit to the company. This applies regardless of intent – the company or a shareholder can sue to recover those gains. Accurate and timely Form 4 reporting helps establish a clear record of when transactions occurred.

Ready to File?

ACN’s insider filing service is fast, simple, and cost-effective. We’ll help you meet your SEC reporting obligations without added stress. Contact us to get started.

Disclaimer: The information provided in this blog post is for general informational purposes only and does not constitute legal, compliance, or financial advice. ACN Solutions LLC is not a law firm, compliance advisor, or affiliated with the Securities and Exchange Commission (SEC). While we strive to provide accurate and timely guidance based on publicly available SEC resources, we do not speak on behalf of the SEC and are not authorized to interpret its rules or policies. Readers should consult their legal counsel or compliance professionals for specific guidance related to their regulatory obligations.